Our recent article, Swaps and Basis Trades Warn Of Mounting Liquidity Problems, touched on negative interest rate swap spreads as an omen of potential liquidity problems. To stay on the topic of liquidity, we didn’t provide much detail about swaps. Nor did we discuss their importance to the financial system. Accordingly, we ended the discussion as follows:

Given the complexity of interest rate swaps and their importance to the plumbing of the entire financial system, we will discuss them further in a coming article.

Shockingly, given that we thought readers would find interest rate swaps dull or wonky to most readers, we have received a few emails asking for more information. Given the importance of liquidity to all markets and how interest rate swap spreads are a good liquidity barometer, it’s worth giving you that “coming article” now.

The Interest Rate Swap Markets

For those who didn’t read our prior article, we share context about the size of the interest rate swap markets.

For a proper framework, the approximate total market cap of the U.S. stock market is $50 trillion, and the global stock market, including the U.S., is about double that. Furthermore, the global bond market is approximately $133 trillion.

As shown below, the notional value of all outstanding interest rate swaps is approximately $575 trillion or more than double the combined value of the global bond and stock markets!

What Are Interest Rate Swaps?

Interest rate swaps are derivative contracts in which two counterparties agree to swap a series of cash flows over a set schedule for a defined term.

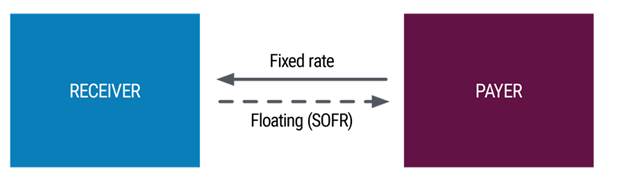

Most commonly, one party agrees to make periodic payments at a fixed interest rate and, in return, receives floating-rate payments. The counterparty receives the fixed payments and pays the floating rate.

Dealers quote interest rate swaps as either the yield on the fixed rate side of the agreement or the difference between the fixed rate yield and that of an equivalent duration U.S. Treasury bond. The latter, which is more common, is called the swap spread.

The floating-rate leg is commonly based on the daily Secured Overnight Financing Rate (SOFR). SOFR, the recent replacement for LIBOR, is the interest rate banks pay or receive from each other to borrow or lend money overnight, with U.S. Treasury securities serving as collateral. Because US Treasury assets secure such overnight borrowing, SOFR is essentially a risk-free overnight interest rate. SOFR typically trades slightly below the Fed’s targeted Fed Funds rate. Fed Funds are unsecured overnight loans between banks; thus, they involve some credit risk.

It’s worth sharing that there are many other types of swap contracts. Here are a few of the more complex agreements, courtesy of Grok.

Digging In Deeper

To better appreciate a “plain vanilla” interest rate swap contract, we analyze a hypothetical ten-year annual paying interest rate swap. As we were writing this article, the ten-year swap spread was trading at -26 bps. The swap rate was 4.14%, 26 basis points less than the ten-year UST (4.40%).

Accordingly, the pay fixed side (payer) will pay 4.14% annually for ten years. In return, they receive the daily compounded SOFR rate. Conversely, the other counterparty, the receiver, will receive 4.14% annually and pay the daily compounded SOFR rate. Instead of payments being made by both counterparties, payments are netted out. Thus, only one party makes a payment at each payment interval.

The payment periods can be monthly, quarterly, semi-annually, or annually. Interest rate swaps can be tailored to the demands of both counterparties. This can include the amount and type of collateralization underlying the contract. Furthermore, it’s common to add basis points to the receiving side of the swap to offset credit concerns. For instance, the agreement may have a swap spread of -26 bps and the SOFR rate plus 12 bps.

When pricing a swap, the fixed rate is determined by calculating the forward value of the daily SOFR overnight rates over the entire swap term. As a result, both sides are entering into a contract based on the current market pricing of expected daily overnight rates for the next ten years.

The illustration and definition below are courtesy of Pimco:

At the time a swap contract is put into place, it is typically considered “at the money,” meaning that the total value of fixed interest rate cash flows over the life of the swap is exactly equal to the expected value of floating interest rate cash flows.

Who Uses Swaps And Why?

Interest rate swaps are speculative vehicles and vital risk management tools. We share details of how and why some of the largest swap traders use them. However, plenty of other types of participants and users exist.

Speculators:

Unlike buying a bond with cash, an interest rate swap is a derivative contract. Thus it requires only a small amount of up-front cash or collateral. Accordingly, a speculator can effectively make a leveraged bet on interest rates, requiring little capital.

For example, an investor with $100 million can buy a ten-year bond. By doing so, they would forgo the money market yield on the cash but earn the bond return. Effectively, they will receive the bond’s fixed rate payment and pay, via opportunity cost, the money market yield.

Alternatively, instead of using cash, the investor can enter a swap agreement to receive a ten-year fixed yield and pay the floating rate. Not only would the return profile versus the opportunity cost (money market rates) look like the cash-bond investment, but after posting a small amount of collateral, the speculator would still have most of the $100 million to invest in something else. They could also post the entire $100 million of cash as collateral and enter into a much larger interest rate swap agreement. Doing so would give the investor much more exposure to bond yields.

Due to the inherent leverage in swaps, many speculators prefer interest rate swaps over bonds. The benefit of leverage also helps explain why some investors buy swaps at a negative swap spread.

Corporate Treasurers:

Corporations use interest rate swaps to convert floating-rate debt payments into long-term fixed payments synthetically. For example, a company enters a pay-fixed rate/receive-floating-rate swap contract. Alongside the agreement they will issue floating-rate debt or a series of short-term bonds matching the floating-rate component of the swap.

The floating-rate debt makes them a floating-leg payer, offsetting the receive floating portion of the swap. What’s left is the pay-fixed leg of the swap. The series of transactions effectively transforms floating-rate debt into fixed-rate debt.

Since credit risk increases with time, most companies can borrow more cheaply and find better liquidity for shorter-maturity paper. Thus, a swap combined with a series of short-term debt issuances, or a floating-rate bond, allows them to take advantage of short-term market pricing yet lock in a fixed rate for an extended period.

Banks/Interest Rate Risk Management:

Banks are among the most active users of interest rate swaps. Their risk management teams constantly aim to match the duration of their fixed-rate assets (loans and fixed-income securities) with the duration of their debt and deposits. Given that banks tend to use 10x leverage or more, duration mismatches between assets and liabilities can introduce substantial interest rate risk.

For instance, a bank with a weighted average duration of five years on its assets and three years on its liabilities is running a two-year duration gap. To help shrink the gap, the bank could enter into a five-year pay-fixed and receive floating-rate swap. Paying the fixed rate is the equivalent of shorting the bond market. Thus, they are reducing the duration of their assets and, therefore, closing the duration gap.

As an aside, while interest rate swaps help manage interest rate risk, Credit Default Swaps (CDS), a topic for another article, help banks and others manage credit risk.

Why Are There Negative Swap Spreads?

With an appreciation for interest rate swaps and some motivations driving the most prominent players to use them, let’s discuss why swap spreads are currently negative. To reiterate, the swap spread is the difference between the longer-term fixed leg of the trade and an equivalent duration Treasury note or bond.

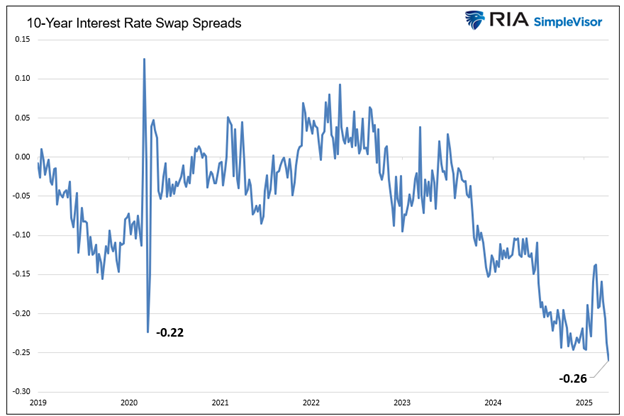

The graph below shows that the ten-year swap spread is at its most negative level in the last five years. Why should the pricing differ by that much if the credit risk and interest rate risk of interest rate swaps and U.S. Treasuries are very similar?

Negative Spread Narratives

Today, there are three popular narratives that we believe are the predominant forces accounting for the negative spread:

- Liquidity/Regulatory

- Deficits

- Speculators Seeking Duration

Liquidity

Banks must hold capital against bond holdings. Thus, when liquidity becomes scarce in volatile markets, they are more likely to buy or sell interest rate swaps versus bonds, as the exposure and impact on their income statements are similar, but the capital requirements are less onerous.

Moreover, it’s often easier and less costly to make a large trade in the swaps market than in the bond market.

In Swaps And Basis Trades Warn Of Mounting Liquidity Problems we wrote:

Banks are forced to sell Treasury securities to raise needed capital, i.e., increase their liquidity. Doing so creates a duration mismatch between their assets and liabilities. Therefore, to manage interest rate risks, they enter into interest rate swap agreements to maintain the duration of their assets. As the demand to receive the fixed rate mounts, the swap rate (rate on the fixed-rate leg of the swap) trades lower. Today, it sits below Treasury rates, thus at a negative spread to Treasuries.

Due to capital requirements, liquidity, and trading costs, paying a premium for swaps, i.e., a negative spread, can make sense.

Deficits

We asked a contact at a significant derivatives dealer why swap spreads were getting more negative and received the following email answer:

“Everyone thinks/knows that the fiscal deficit will get worse. Trump’s election did nothing to dissuade that. Higher deficits…more U.S. Treasury issuance…higher U.S Treasury yields.”

When asked about other factors, he opined that his bank thought 90% of the swap spread discount versus Treasury securities was deficit-related.

Essentially, our friend believes investors are concerned that higher deficits will result in more debt issuance. Therefore, investors are pushing yields on Treasury securities higher as they demand a “term premium” to protect them from the extra supply. Swap levels are not directly impacted by greater debt issuance.

Jeff Snyder’s Opinion – Duration Buying

Next, we watched a YouTube video of Jeff Snyder, an expert on the interest rate swap markets. He states the following:

“All swaps tell us is that the market is strongly forecasting rates to go down and stay there. We have to fill in the blanks for what that might mean, and there is no one scenario which would fit. This could be a recession, but even that can lead to multiple different near-term outcomes which eventually converge in the future the swap market has projected. The global economy has already moved in the way swaps were pricing despite so many doubts – including many who said inflation would force rates forever higher.”

Jeff argues that speculators are buying duration via the swap market. While the fixed rate on swaps is lower than similar duration U.S. Treasury yields, swap payers need little cash, as we noted earlier. Thus, the benefits of the leverage more than offset the lower yield. Furthermore, liquidity in the interest rate swap markets is plentiful.

Summary

Oftentimes, liquidity problems show up in the more popular stock and bond markets well after they expose themselves in other markets, such as interest rate swap agreements. As we graphed, interest rate swap spreads have declined into negative territory for over three years.

If liquidity were plentiful, and thus leverage cheap and easy to attain, why would someone agree to receive 26 basis points less via a swap than a cash bond?